Financial Challenges Faced by Newcomers in Canada And Why Mentorship Matters

Starting a new life in Canada is exciting, but the financial side can be overwhelming. Newcomers arrive with big goals and strong work ethic, yet they face a financial system that looks and behaves very differently from what they knew back home. Surveys now show that newcomers lose confidence after arrival, worry about making mistakes, and struggle to find trusted guidance.

By Gabriel / May 16, 2026

Starting a new life in Canada is exciting, but the financial side can be overwhelming. Newcomers arrive with big goals and strong work ethic, yet they face a financial system that looks and behaves very differently from what they knew back home. Surveys now show that newcomers lose confidence after arrival, worry about making mistakes, and struggle to find trusted guidance.

This is exactly where having a financial mentor or advisor becomes a game changer.

The confidence drop after arrival

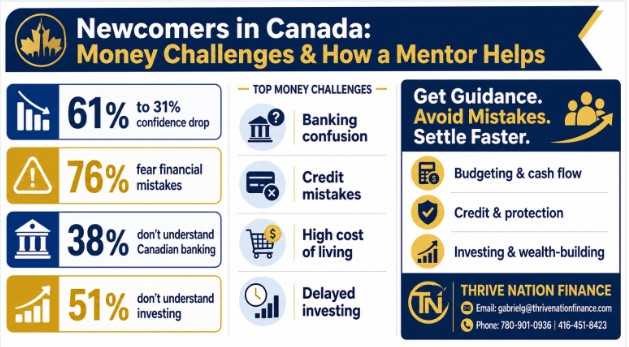

Research shows that newcomers start out hopeful, then hit a confidence wall once they confront Canada’s real costs and complex financial system. An Interac survey found that 61% of newcomers felt financially confident when they arrived, but that dropped to just 31% after they faced the realities of settling here.

In the same research, 85% of newcomers said at least one financial barrier affects their financial security, compared with 58% of the general Canadian population. This means most newcomers are dealing with real obstacles, not just minor inconveniences.

A TD survey paints a similar picture:

- 38% of newcomers reported little to no understanding of the Canadian banking system and how to manage their money here.

- 51% reported little to no understanding of investing money in Canada.

- 41% said they had little to no understanding of the Canadian economy.

On top of that, 76% of newcomers said they fear making a financial mistake, and 35% said they feel embarrassed or judged when they seek financial help.

So the issue is not laziness or lack of ambition; it is a confidence and knowledge gap in a completely new environment.

Major financial pressures for newcomers

1. High living costs and tight budgets

The Government of Canada notes that housing, utilities, food, and transportation can easily take 35–50% of household income, and sometimes more. Newcomer-focused cost-of-living guides show that a single person in a large city can easily face monthly costs in the $2,000–$3,500+ range, depending on housing and lifestyle.

What makes this harder is that many newcomers also:

- Support family back home.

- Pay for language training or credential recognition.

- Face employment under-matching in the early years.

All of this squeezes their ability to save, invest, or absorb mistakes.

2. Banking confusion and hidden costs

Newcomers often find Canadian banking confusing: which account to open, which fees to avoid, and how online banking, e‑transfers, and bill payments work. Scotiabank-commissioned research and newcomer guides highlight top issues such as:

- Unclear documentation requirements to open an account.

- Confusion around monthly fees, ATM charges, and foreign transaction fees.

- Difficulty understanding overdraft, minimum balance rules, and transfer limits.

When people don’t know the rules, they pay the price in unnecessary fees and stress.

3. Credit-building mistakes that slow settlement

Credit is one of the most misunderstood parts of the system. Newcomers typically arrive with no Canadian credit file, which affects renting, borrowing, and sometimes even job screening. Common early mistakes include:

- Missing payments (even once) on a new card or phone bill.

- Maxing out a card or using more than about 30% of the limit.

- Applying for multiple cards in a short period.

- Closing their oldest card too quickly.

Because payment history and utilization are major parts of a credit score, one or two missteps early can hold someone back for years.

4. Delayed or avoided investing

TD’s survey found that 51% of newcomers reported little or no understanding of investing in Canada. Unsurprisingly, many delay investing because they:

- Don’t understand TFSA, RRSP, FHSA, or how taxation works on investments.

- Fear making a wrong move when markets feel unfamiliar.

- Are still trying to stabilize income, housing, and credit.

The result is that newcomers often stay in “cash only” mode for years and miss valuable compounding time.

5. Insurance gaps and vulnerability

Securian Canada’s newcomer research found that many are uninsured or underinsured, which raises vulnerability: around 60% of surveyed newcomers were underinsured, and about 20% had no coverage at all. Financial stress was highest among underinsured newcomers (58%), compared with 48% among those who were insured.

At the same time, newcomers said they were:

- Unsure who to turn to for guidance.

- Worried about being misled.

- Struggling to access professional advice.

Insurance is one area where “not knowing” can be very expensive when something goes wrong.

The role of a mentor or advisor

When you look at the data, a pattern emerges: newcomers are motivated and ambitious, but held back by system-specific knowledge gaps and fear of mistakes. Surveys show they want to be financially stable and plan for the future: TD found newcomers’ top priorities included preparing for uncertainty (40%), investing effectively (37%), saving for retirement (36%), and being debt-free (32%).

This is exactly where a mentor or advisor makes the biggest difference.

A good mentor or advisor can help a newcomer:

- Understand Canadian banking and choose the right low-fee account.

- Create a realistic settlement budget that covers both obvious and hidden costs.

- Build credit the right way from day one (autopay, low utilization, patient growth).

- Decide when to start investing and which simple, diversified options fit their goals.

- Navigate life and health insurance choices without being over- or under-sold.

Given that 76% of newcomers fear making a financial mistake and 35% feel embarrassed seeking help, having a trusted, culturally aware advisor who understands both their background and Canada’s system is incredibly valuable.

How Thrive Nation Finance supports newcomers

For newcomers and international students who want structured support instead of trial-and-error, Thrive Nation Finance positions itself as a practical guide.

According to its site, Thrive Nation Finance focuses on:

- Personal and home finance guidance.

- Budgeting and cash-flow planning.

- Investment education and long-term wealth-building strategies.

- Credit improvement and understanding Canadian credit systems.

- Retirement planning and future-focused financial strategies.

- Education-first support so clients truly understand the “why” behind each decision.

This education-first approach responds directly to the gaps identified in the surveys: low understanding of banking and investing, high fear of mistakes, and difficulty finding trustworthy advice.

Who Thrive Nation Finance serves

Thrive Nation Finance serves:

- Individuals who want help with day-to-day money decisions.

- Families building budgets, savings, and long-term stability.

- Newcomers and immigrants who need Canada-specific financial education.

- People aiming to improve credit, plan for retirement, or build wealth over time.

The emphasis is on clear, approachable guidance rather than product-pushing, which is exactly what many newcomers say they want.

How to contact Thrive Nation Finance

From its website, the primary contact details are:

- Email: gabrielg@thrivenationfinance.com

- Phone: 780-901-0936

- Phone: 416-451-8423

Email is often the best first step for newcomers because it allows them to explain their situation in their own time and language, and receive guidance tailored to their needs.

A simple roadmap for newcomers

Putting all this together, a practical settlement roadmap looks like this:

- First 90 days

- Open a suitable low-fee account.

- Start a basic budget for rent, food, transit, phone, and remittances.

- Get a starter or secured credit card and set up autopay.

- Months 3–12

- Build a small emergency fund.

- Keep utilization low and avoid missed payments.

- Learn TFSA/RRSP basics and start small, regular investing once cash flow allows.

- Year 1–3

- Review insurance needs (life, disability, tenant, etc.).

- Strengthen credit and consider longer-term goals such as home ownership or business.

- Refine investing strategy for retirement and other goals.

At every stage, working with a mentor or advisor significantly reduces costly mistakes and speeds up progress.

Key message for newcomers

The research is clear:

- Confidence drops from 61% to 31% after arrival.

- 38% don’t understand banking, 51% don’t understand investing.

- 76% fear making a financial mistake.

- Many are underinsured and unsure whom to trust for guidance.

So if you feel overwhelmed, you are not alone and it is not a sign of failure. It is a signal that you are navigating a complex system without a map.

Having a mentor or advisor, such as Thrive Nation Finance, gives you that map. With the right guidance, you can avoid the most common traps, settle faster, and start building the financial future you came to Canada for.